TRIPLE TAX BENEFIT

HSA and FSA

Health Savings Account (HSA)

Tax-free Saving and Spending

Benefit Decision Tool

If you can imagine a financial product that provided tax-free income, tax-free growth, and tax-free spending, then you can imagine the amazing Health Savings Account (HSA):

Tax-free Income

That's right! If you participate in a qualified High Deductible Health Plan (HDHP), you qualify for tax-free income. Money deposited into your HSA, from either Verra Mobility or you, is money that is not subject to regular federal income tax. And, in most states, the money is also not subject to state income tax. *

* HSA deposits are pre-tax, with respect to federal income tax. But not all states recognize HSA deposits as pre-tax against their respective state income taxes. States that do not permit HSA pretax deductions include,

1. California

2. New Jersey

Please check with your personal tax advisor to learn how your state treats HSA deposits for state income tax purposes.

Tax-free Earnings

Many people do not realize, they can invest their excess HSA funds, just as they would a 401(k).

Yes, it's true. With an HSA plan, you are permitted to set aside a portion of your HSA and invest it in various investment vehicles, such as mutual funds and bonds. Better yet, growth in value of these investments happens tax-free! This tax-free growth is tremendous for your rate of return!

Tax-free Spending

You read that right! You may spend your HSA money at any time. And money spend for eligible expenses - essentially medical, dental, and vision out-of-pocket, eligible expenses - can be purchased with your HSA funds without being subject to tax.

The Learn More button takes you HealthEquity's explanation of what expenses are eligible with your HSA.

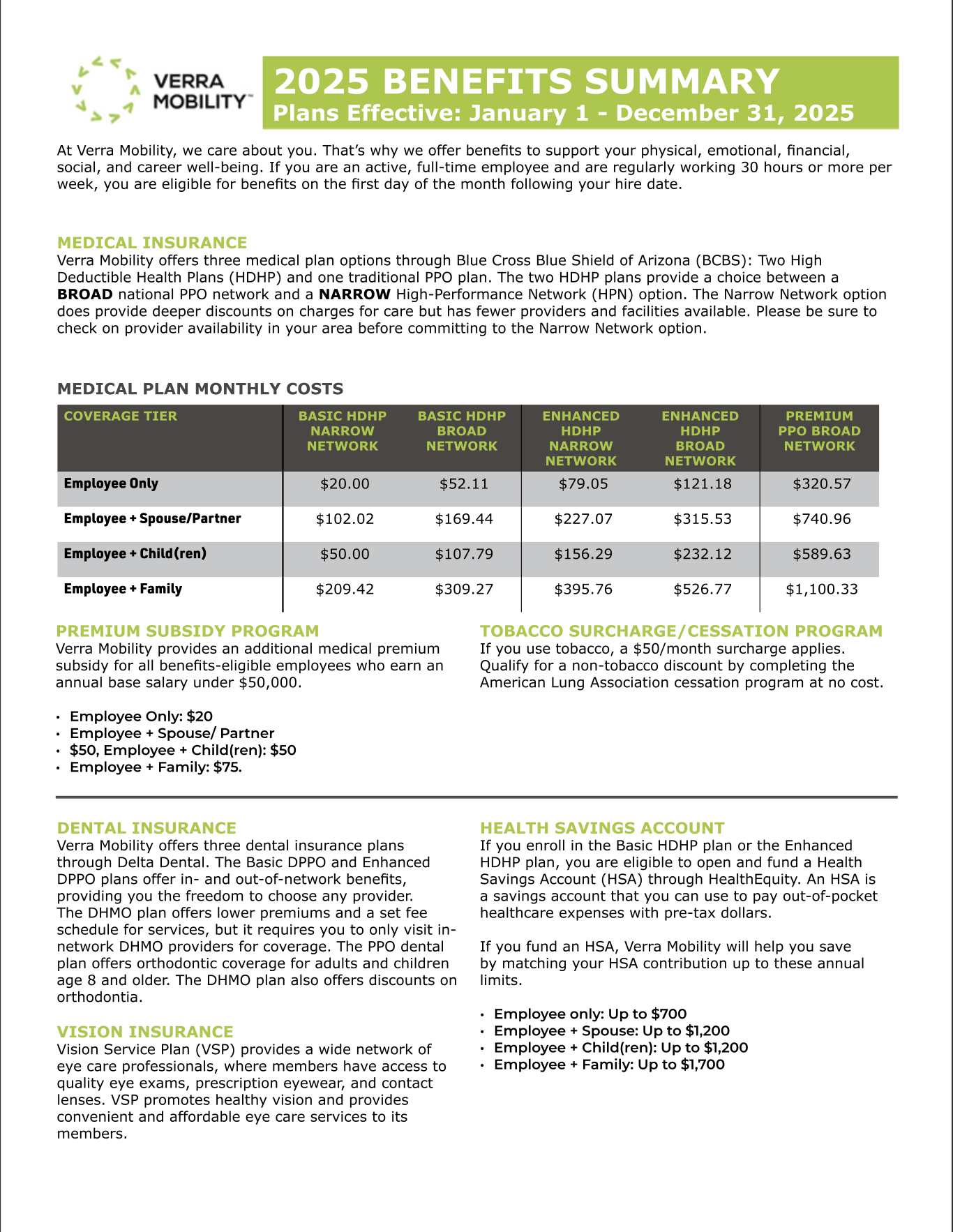

HSA Limits for 2025

It's important to stay informed about the contribution limits for Health Savings Accounts (HSAs) and the requirements for High-Deductible Health Plans (HDHPs). For those with self-only coverage, the contribution limit will be $4,300, while families can contribute up to $8,550. If you are 55+, you are permitted to deposit an additional $1,000 into your HSA.

Note: The above limits are from all sources. Specifically, Verra Mobility matches your contributions toward your HSA (please see below for more details). Therefore, the maximum contribution limit is the combination between the amount you and Verra Mobility contribute toward your account.

What is an HSA?

A Health Savings Account (HSA) is a tax-advantaged account that allows you to save for medical expenses. It works in conjunction with a High-Deductible Health Plan (HDHP) and offers benefits like tax-free contributions and withdrawals for qualified medical expenses.Who can contribute to an HSA?

Anyone enrolled in a qualified HDHP can contribute to an HSA. This includes individuals with self-only or family coverage. Contributions can be made by the account holder, their employer, or anyone else on their behalf.Does Verra Mobility make a contribution toward my HSA?

If you enroll in the Basic HDHP or Enhanced HDHP, Verra Mobility will help you save by matching your HSA contribution. This contribution will be pro-rated and will occur in every paycheck. For new hires, Verra Mobility’s first contribution will be made within the first pay period after you are benefits-eligible.

Below is a breakdown of Verra Mobility's contribution match.

- Employee only: Up to $700

- Employee + spouse: Up to $1,200

- Employee + child(ren): Up to $1,200

- Employee + family: Up to $1,700

What are the tax benefits?

HSAs offer triple tax benefits: contributions are tax-deductible, the account grows tax-free, and withdrawals for qualified medical expenses are also tax-free. This makes HSAs a powerful tool for managing healthcare costs.Can I deposit to an HSA and have another plan, like an FSA?

No. You are not allowed to enroll and contribute toward the traditional Health Care FSA, while also being enrolled in the HSA. There is an FSA that is compatiable with your HSA. You may only enroll and contribute toward a Limited Purpose FSA along side your HSA.

Do I lose my money if I don't use the funds at the end of the year?

No. Unlike the FSA where the funds are use it or lose it, funds in the HSA rollover from year to year.

Flexible Spending Accounts

Flexible Spending Accounts (FSAs) are employer-sponsored benefit plans that allow employees to set aside a portion of their pre-tax income to pay for eligible medical expenses and dependent care expenses.

Health Care FSA

The Health Care Flexible Spending Accounts (FSA) can be used to cover a wide range of expenses, including co-pays, deductibles, prescription medications, and certain over-the-counter items. Health Care FSAs offer a tax advantage by reducing taxable income and can help individuals save money on out-of-pocket healthcare costs.

Limits

As of 2025, the Health Care FSA contribution limits is set at $3,300 per year. These limits are subject to change based on inflation and other factors. It is always recommended to check with your employer or FSA administrator for the most up-to-date information on contribution limits.

Rollover

Funds remaining in the Health Care FSA will rollover to the following year. Any funds that exceed $660 will be lost. You have 90 days after the end of the year to submit for reimbursement for the current year expenses.

To avoid overfunding your Health Care FSA, carefully consider your regular out-of-pocket, eligible medical expenses and best estimate what you may spend in 2025.

Limited Purpose FSA

A Limited Purpose Flexible Spending Account (FSA) is a type of account that allows you to set aside pre-tax dollars to pay for eligible medical expenses.

Unlike a traditional Health Care FSA, a Limited Purpose FSA has restrictions on the types of expenses that can be reimbursed, typically only covering specific expenses such as dental and vision care.

Limited Purpose FSAs are often offered in conjunction with a high-deductible health plan and are subject to annual contribution limits set by the employer. Any funds left in a Limited Purpose FSA at the end of the plan year may be forfeited, so it's important to plan expenses carefully.

Limits

As of 2025, the Limited Purpose FSA contribution limits is set at $3,300 per year. These limits are subject to change based on inflation and other factors. It is always recommended to check with your employer or FSA administrator for the most up-to-date information on contribution limits.

Rollover

Funds remaining in the Limited Purpose FSA will rollover to the following year. Any funds that exceed $660 will be lost. You have 90 days after the end of the year to submit for reimbursement for the current year expenses.

To avoid overfunding your Limited Purpose FSA, carefully consider your regular out-of-pocket, eligible medical expenses and best estimate what you may spend in 2025.

Dependent Care FSA

A Dependent Care Flexible Spending Account (DFSA) is a pre-tax benefit account that allows employees to set aside money to cover eligible dependent care expenses. These expenses typically include child care, day care, preschool, summer day camp, and before or after school care for children under the age of 13, as well as care for elderly or disabled dependents.

Employees contribute a portion of their pre-tax salary to the Dependent Care FSA, which can then be used to reimburse themselves for eligible expenses. This can result in significant tax savings, as the contributions are not subject to federal income tax, Social Security tax, or Medicare tax.

Limits

The DFSA limit is $5,000 per household, or $2,500 if married and filing separately. This limit is subject to change based on inflation and other factors. It is always recommended to check with your employer or FSA administrator for the most up-to-date information on contribution limits.

Use It Or Lose It

It's important to note that funds in a Dependent Care FSA are "use it or lose it," meaning that any unused funds at the end of the plan year are forfeited. However, some employers may offer a grace period or carryover option to allow employees to use up remaining funds.

Using Your FSA, LFSA, or DFSA

Filing an expense reimbursement claim with your Flexible Spending Account (FSA) with HealthEquity is a straightforward process, though it comes with a few essential steps. Typically, you'll need to gather itemized receipts and complete a reimbursement form, ensuring that your expenses align with FSA guidelines.

What To Keep and Submit

When using your HealthEquity debit card, keep in mind, the administrator is going to require submission of supporting documentation.

Your documentation or receipt must include:

- Provider name on their own receipt or paperwork

- Date of Service

- The description of the qualified expense

- The amount charged

Most providers of services are keenly aware of these requirements, and their regular receipts and documentation are careful to denote these elements.

In most instances, you can easily submit your documentation by submitting a picture of the document using HealthEquity's mobile application.

Get HealthEquity Mobile App

Commuter Benefits

Commuter benefits allow you to put money from your paycheck aside each month,

before taxes are taken out, for qualified mass transit and parking expenses.

What does it cover?

Commuter funds can be used on a variety of transportation and parking expenses that allow you to travel to and from work. Eligible modes of transportation include but aren’t limited to:

- Train or Ferry

- Bus or Subway

- Vanpool (must seat at least 6 adults)

- Parking or parking meter near your place of employment

Maximum Contributions

- Commuter Transit: $325

- Commuter Parking: $325

Contribution changes

You can adjust the amount you contribute to the plan each month at any

time. No qualifying event is needed.

Rollovers and use-or-lose

The commuter plan is flexible and your funds will continue to roll over month to month until the funds are used. However, your funds will no longer be available if you terminate employment